School of Business and Industry,

Florida A&M University

"Randomized objective function and constraint limit linear programming in risk management"

Jan 27, 2021 Schedule:

- Virtual Tea Time

- 03:00 to 03:30 PM Eastern Time (US and Canada)

- Virtual Colloquium

- 03:30 to 04:30 PM Eastern Time (US and Canada)

Abstract:

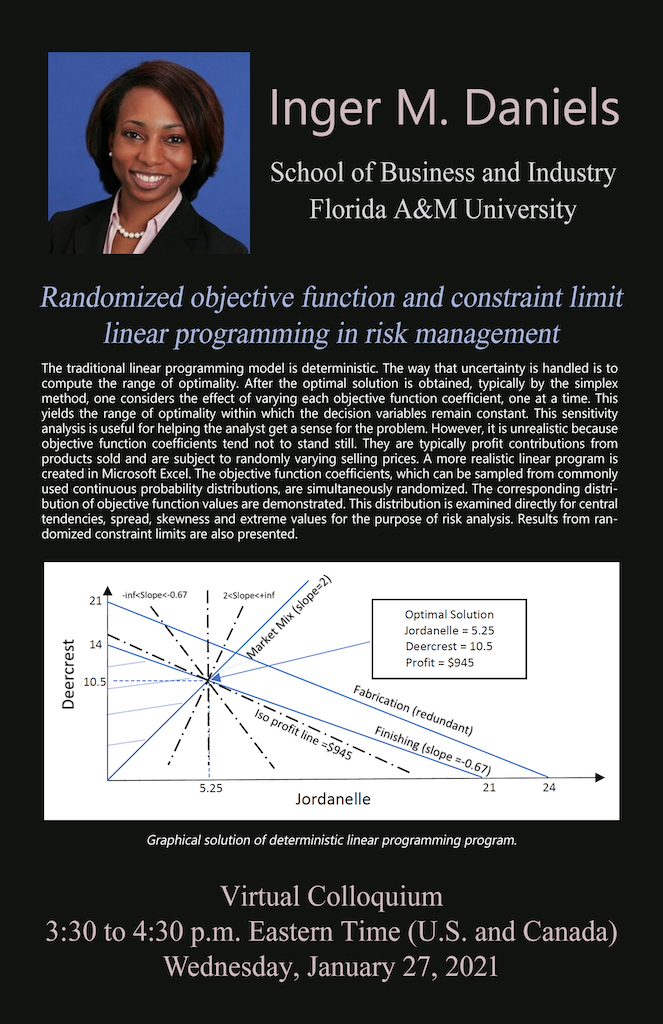

The traditional linear programming model is deterministic. The way that uncertainty is handled is to compute the range of optimality. After the optimal solution is obtained, typically by the simplex method, one considers the effect of varying each objective function coefficient, one at a time. This yields the range of optimality within which the decision variables remain constant. This sensitivity analysis is useful for helping the analyst get a sense for the problem. However, it is unrealistic because objective function coefficients tend not to stand still. They are typically profit contributions from products sold and are subject to randomly varying selling prices. A more realistic linear program is created in Microsoft Excel. The objective function coefficients, which can be sampled from commonly used continuous probability distributions, are simultaneously randomized. The corresponding distribution of objective function values are demonstrated. This distribution is examined directly for central tendencies, spread, skewness and extreme values for the purpose of risk analysis. Results from randomized constraint limits are also presented.

| File | Description | File size |

|---|---|---|

2021-01-27daniels.jpg 2021-01-27daniels.jpg | Advertisement | 515 kB |